Everyone knows that lower interest rates make it easier to borrow to purchase a home, but how much of the recent price appreciation in Bay Area housing can we attribute to lower interest rates and what is ahead for housing prices?

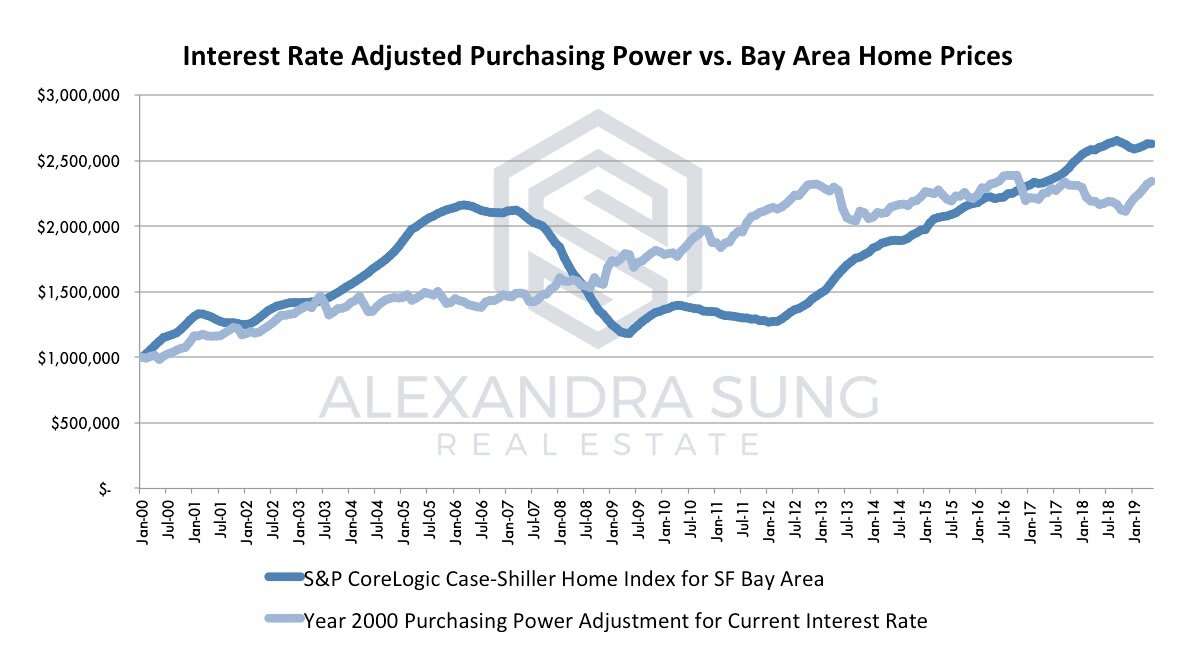

To tackle these questions, I used the Case-Shiller index for pricing data since 2000 and compared it to the cost to borrow over the same time period. Suppose an individual bought a home in 2000 in Silicon Valley for $1 million and financed 80%, or $800K. The annual principal and interest expense using the prevailing mortgage rate (approx. 8%) would have been $71,852. Taking that annual cost for principal and interest and growing it with inflation (using the Consumer Price Index as an approximation), we can back into how much purchasing power increases as interest rates drop. The annual spending on principal and interest increases modestly each month from 2000 to present day, but because interest rates are dropping and because mortgages provide leverage, the increase in the value of a house one can afford is disproportionate. Purchasing power increases significantly with the drop in interest rates:

Sources: 30 year fixed rate mortgage rates and S&P Core Logic Case-Schiller Index for San Francisco Bay Area home price data taken from Federal Reserve Bank of St. Louis FRED Economic Data

Someone who bought a $1 million house in 2000 can afford a $2,342,336 house today. Moreover, with the increase in popularity of adjustable rate mortgages, a buyer can tap into even lower interest rate boosting his or her purchasing power further. The Case-Shiller index indicates that a $1 million house in 2000 would be worth $2,627,757 today. This implies that less than $300K of the appreciation is due to factors other than interest rates, such as supply-demand dynamics.

Looking ahead, the graph may also provide some insight into the future for Silicon Valley housing prices. When housing prices significantly exceeded purchasing power such as between 2004 and 2007, there was a subsequent correction, and when purchasing power significantly exceeded housing prices such as between 2009 and 2016, there was a subsequent rapid rise in housing prices. Currently, there is a small delta between housing prices and purchasing power, suggesting that we are at near equilibrium with a possible slight correction in store.

As always, there are some limitations to this analysis. I have focused on interest rates and thus the principal and interest component of total housing expense, but it is important to note that property taxes and insurance are additional expenses for homeowners. Moreover, there remains a significant obstacle for first-time homebuyers attempting to enter the market. With 20% down, a first time homebuyer in 2000 needed $200K for a $1 million house. Even with the (S&P) market return on $200K since 2000, a first-time homebuyer would still be around $130K short to purchase a $2.6M home today with 20% down. Stock and options have provided a means to a down payment for many in the Bay Area, but this does pose a risk to the market should a pullback cause a significant decline in the financial markets.

Obviously, there are other nuances involved in the day-to-day changes in housing prices and there may remain discrepancies between housing prices and purchasing power for protracted periods of time. However, in a desirable place to live like the Bay Area, falling interest rates appear to account for the lion’s share of the current run up in housing prices. Furthermore, interest rates should remain flat to slightly lower in the near future, not only because of the recent weakened economic outlook, but also due to a shift to more mortgages backed by non-bank investors, who are driven by free market forces. These factors act as a mitigating factor for any near-term continued softening in the housing market and make a significant pullback like the one we experienced in the last recession unlikely.